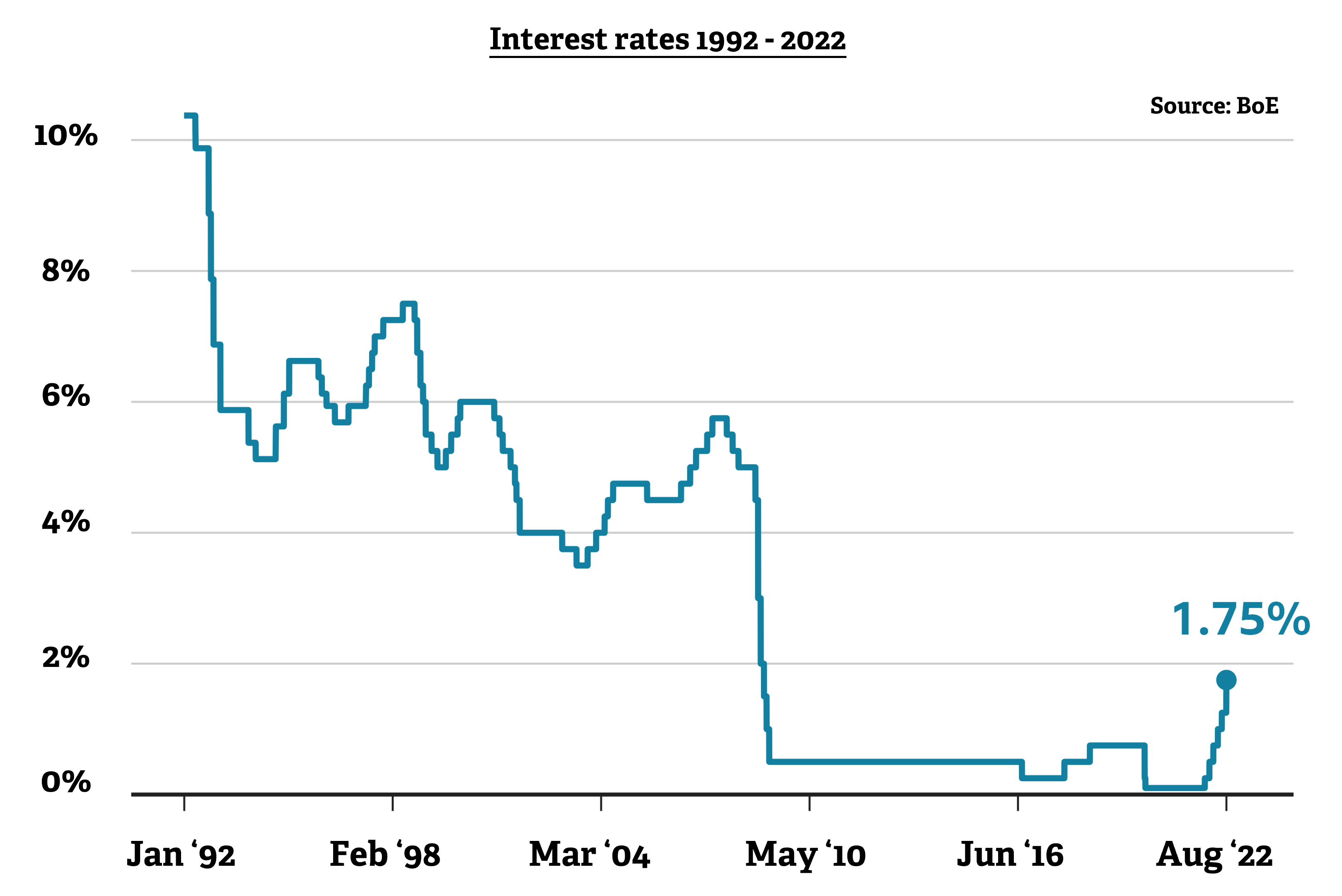

The Bank of England raised interest rates by 0.5% last week, the greatest single rise we have seen in 27 years, taking the base rate to 1.75%. So what does this mean for the property market?

Firstly, it’s important to recognise that despite the rises seen over the past few months we are still in an astonishingly low interest rate environment. When I got my first mortgage I would’ve bitten your arm off for a rate of 3.49% fixed for five years (widely available in the current market) and actually felt quite grateful for the 6.0% I was paying in comparison to the home movers securing finance just a few years before I ventured onto the property ladder. Nevertheless for anyone who has got mortgage in the past 12 years, this is a significant shift which will no doubt have an impact on affordability for many. The cost of borrowing, however it’s just one of three primary factors which drive the housing market with the other two being supply and demand. The past two years has seen demand at record levels and whilst there is no doubt we have seen a slight softening in the past two to three months, new buyer registrations are still at significantly higher levels than they were pre-Covid and continue to defy expectations. At the same time the supply of new housing stock to market has been restricted for at least two years and the inertia in more properties coming to the open market suggests it will be like this for some time which continues to fuel competition amongst buyers at all price ranges. This imbalance of supply and demand is unlikely to change in the short term despite inflationary pressures and predictions of further rate rises over the coming months. The most astute in the market appreciate the direction of travel and are looking to get a mortgage product now and fix the rate for five years as it is only likely to cost more to borrow the same amount in the coming months.

Sellers, waiting to ‘see what happens’ are likely to find themselves at a disadvantage especially if they’re looking to trade-up in the market. Now is the time to secure a strong price on your sale, lock-in finance and put yourself in a position to be able to transact quickly when the best property for you comes to market. As a landlord, any increase in borrowing cost is highly likely to be mitigated by rents at the highest we have ever experienced as a stock-starved market encourages renters to compete to secure properties.

If you haven’t spoken to a mortgage broker in the past couple of weeks it is likely your borrowing capacity and subsequent repayments will have shifted so it’s important to reassess your position now to give yourself the competitive edge against others in the market and not find yourself disappointed when your perfect property drops onto the market.